Death by Fundraising

Death by Fundraising

A guy starts a company and invests $1bn. The company is worth $1bn. A startup guy starts a company, creates a great product and seduces millions of users. The company is worth $300M. WTF happened?

A guy starts a company and invests $1bn. The company is worth $1bn. A startup guy starts a company, creates an insanely great product, hires a stellar team, and seduces millions of users. The company is worth $300M. WTF happened?

The startup guy got capital killed, a slow and painful death by fundraising.

It's a mega bull market; no day passes without announcements of record fundraising coupled with skyrocketing valuation. Time to get rich quick!

On the other hand, veteran investors warn how hard it is to earn returns in startup investing. Garry Tan commented, "I never really paused to consider how rare it is for venture capitalists to actually be successful at what they do." Oops, I thought it was easy!

Venture capital (VC) is a form of private equity financing. To invest in high-growth potential startups, VC firms pool money from limited partners (LP) who are high-net-worth or institutions like pension funds or university endowments. Because of the significant risk, LPs expect a rate of return of at least 3x, meaning a $100 million fund has to return $300m.

VC firms' returns follow a steep power law. Andy Rachleff, the co-founder of Benchmark, a top-tier VC firm, writes that "about 3 percent of the universe of venture capital firms – generate 95 percent of the industry's returns." There is also a strong path dependence where "the composition of the top 3 percent doesn't change very much over time."

In short, most VC firms barely return investors' money after fees, while the best firms tend to seize all the returns. Looking at recent data, Seth Levine notes that "despite the historic market we've had in the past ten years, and the huge deals often highlighted in the press, venture capital returns haven't shifted much."

VC firms need billion-dollar acquisitions to match the expected returns. Most VC investments will come at a loss, and only billion-dollar outliers can cover the loss and, hopefully, generate returns. Even Ron Conway's angel fund, which invested in seed in Google, only broke even - meaning a 0% IRR. This business is extra tough!

The recent bull market led VCs to fund companies with a lot of money in the hope of creating monster businesses. The more capital, the better. Massive fundraising rounds are celebrated, and unicorn entrepreneurs are on magazine covers. The bigger the better right?

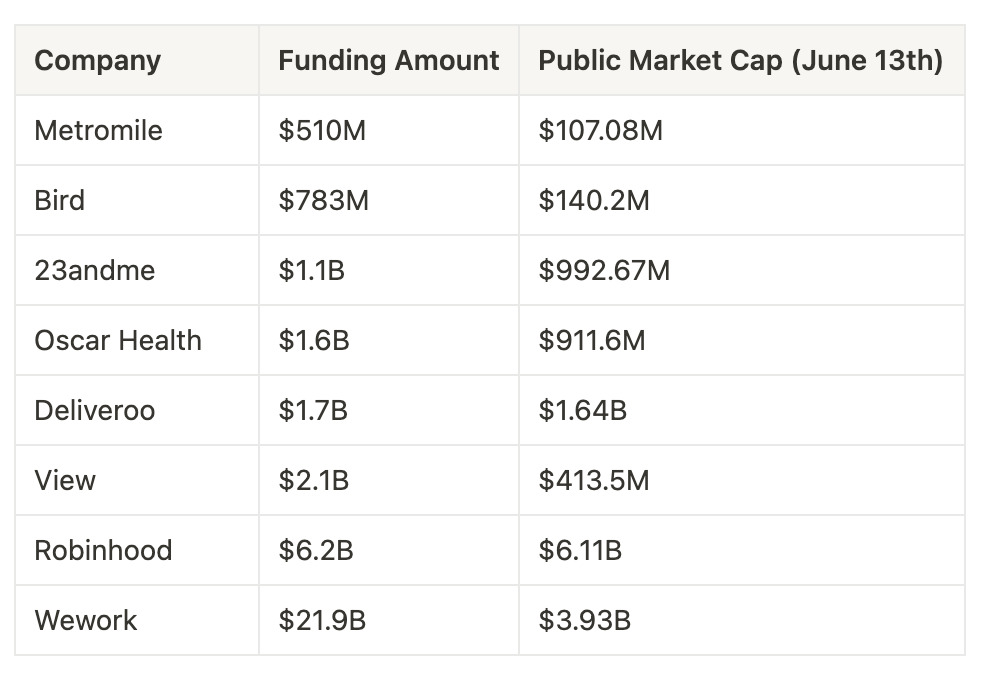

Let's consider these startups. They all have raised more money than their public market valuation in June 2022.

Now, industrial failure happens. It's even the common state as most startups go bankrupt. However, my point is that these "good" businesses became "terrible" businesses because of their fundraising strategy.

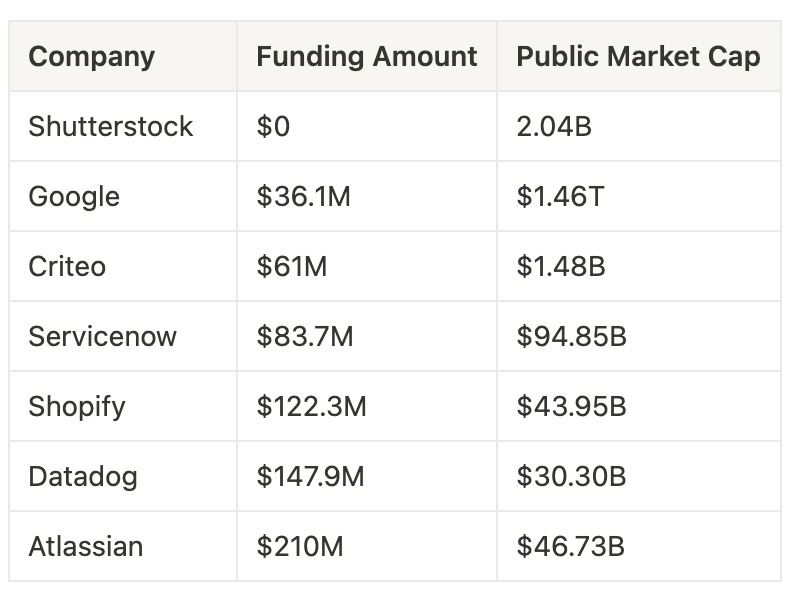

Breaking news: one can build a monster business without tons of capital infusion.

Additionally, entrepreneurs and their teammates don't need to raise money to be successful. There are plenty of great bootstrapped startups. Some of them are selling for billions of dollars, such as Mailchimp which sold for $12 billion to Intuit. It's even more likely to experience better financial success with reasonable funding. Quoting Eric Paley: "the Huffington Post was reportedly acquired for $314 million, and Arianna Huffington made about $18 million. Michael Arrington sold TechCrunch to the same buyer for $30 million and reportedly kept $24 million. To a VC, TechCrunch's sale would have been a "loss," and many VCs would have pushed Michael not to sell. Yet Arrington was more successful, financially, than Huffington".

To sum up, it's possible to sell a startup for a billion dollars and make less than someone who sells theirs for $100 million. Alas, many $100 million companies fail because they raised capital as if they would become multi-billion-dollar unicorns.

The above startups built massive businesses without a lot of cash infusion. They focused on cash flows, not raising money. Most of today hot Series C startups have already raised more money. What could go wrong?

Raising too much might kill your startup. While fundraising, most founders get too excited by the economics, namely the dilution, which is a function of the valuation and the amount raised. They forget something essential: terms and conditions.

One of the essential terms is liquidation preferences. It states that in the event of a sale for less than the last valuation, investors and preferred stockholders get their money back first. A 1x liquid pref means that investors who invested $x, must be paid back $x regardless of their equity ownership. Likewise, a 2x liquid pref means that investors must be paid back $2x the invested amount.

Liquid prefs often wipe out the entire cap table. Let's consider an extreme scenario with a startup that raises $10m at a $50m valuation with a 2x liquid pref. If the company sells for $20m, then investors will take 100% of the payout. That's why terms matter more than valuation. Charles Yu wrote an excellent guide to liquidation preferences.

These situations are, unfortunately, all too common. According to a study, 66% of venture-backed startups that exited in the last decade did not return any meaningful capital to management.

It's not unusual, as we have seen, for a startup to sell for less than the amount raised.

We saw in the previous examples that the exit amount is a significant factor in the payout determination. A fundraising strategy should take into account the potential enterprise value at exit. It's, of course, impossible to predict in such an uncertain game, but industry and geographical data can provide perspective. For instance, big exits are concentrated in the US, meaning raising a lot without operating in the US is hazardous.

Another essential factor to keep in mind is the exit multiple and their volatility. Exit multiple is a method of calculating enterprise value using a revenue multiple. These multiples are cyclical, which is dangerous. For instance, the median Private B2B SaaS startup was acquired for 5x its revenue in 2016 compared with 12x today in Oct 2021.

The high exit multiples of today drive higher fundraising valuation, but what if exit multiples go back to their historical average?

The fundamental issue is that the company's fundraising valuation, and terms - aka liquid prefs- won't adapt to the new exit environment. Same for burn rate which is very hard to readjust. A lot of wealth will be destroyed that way.

Suppose a company with a $10M annual recurring revenue (ARR) business. This startup will today raise at 50x revenue (or 100 to 200x here in San Francisco, lol), implying a $500M valuation. The VC valuation is higher than today's potential exit value of $120m (12x median revenue multiple) because the assumption is that the company will grow its revenue and thus create value for the investors. However, if the exit multiples go back to say 5x, even with an incredible performance of $40m in revenue, the company will be only worth $200m at the exit. Oops.

This dramatic example doesn't even discuss that not all growth is created equal. Consuming a lot of capital to create few revenues is a recipe for disaster. As Paul Graham wrote: "If you raise money you don't need, it will turn into expenses you shouldn't have." Some startups are like dead stars, they shine for now, but they are already dead. A good company doesn't need a lot of capital to expand.

The never-ending fundraising rounds often mask an unsustainable business in which every stakeholder is ruined in the end.

Why are there so many fundraising rounds, even if it's a challenging endeavor? The answer lies in the incentives. Venture capitalists have an incentive to deploy their cash. VCs take home a 2% management fee on committed capital, meaning they have an urge to deploy the money and raise a larger fund.

On the other hand, founders want to raise to fuel their business with cash in the hope of defeating competitors. Additionally, employees are pressuring management to raise money because it means higher wages. A big fundraising round is the ultimate form of social status in the startup world. It gives an appearance of success; your partner, friends, and family think that you're successful. As if that wasn't enough, founders nowadays take significant cash out when raising money. It might kill the company tomorrow, but the millions in the bank account today are real.

It's hard to invest or build a successful business; fundraising is a complex and dangerous art that must be thought through carefully. While first-time founders are obsessed with how much they can raise, successful second-time founders wonder "how little money we can raise."

The strategy of raising little money as possible is backed by evidence.

The authors of Overdosing on VC: billion-dollar: Lessons from 71 IPOs noted that: "by examining the technology IPOs of the past five years, we found that the enriched (well-capitalized) companies do not meaningfully outperform their efficient (lightly capitalized) peers up to the IPO event and actually underperform after the IPO. Though increasingly unfashionable in the unicorn era, it is quite possible, and perhaps even advisable, to build a billion-dollar publicly-traded company with under $50M in venture capital."

I'm not against fundraising; my own business raised two rounds led by VC. Venture capital is a fantastic tool to kick off risky business and change the world. The key is to balance the founders' interests and VC's objectives properly because both are not aligned. The other balance to master is that more capital doesn’t mean a better business. Sometimes, cheap capital is available, but it’s better not to take it.

It all depends on the context; in the end, however, nothing beats cash flows. Stay safe out there and think long-term! Leaving the last word to Warren Buffet: "If it seems too good to be true, it probably is."

If you found this article valuable, please consider sharing it 🙌

I've resisted fundraising, possibly to a fault. Your article however articulates precisely why. Thank you.

Great piece of work 🙏